Sun 5 Jul 2009

Nice animated, graphical work over at Tip Strategies to cover unemployment across the US over the last few years…

Sun 5 Jul 2009

Nice animated, graphical work over at Tip Strategies to cover unemployment across the US over the last few years…

Sat 4 Jul 2009

Nicholas Nassim Taleb catches flack from time to time for being a perma-bear. One of my friends even complains that he doesn’t think Taleb is worth listening to because we don’t know if he has made money off his views and predictions, specifically with the hedge fund where he is a principal.

I watched the video below, and it’s obvious to me that Taleb is not a trader, nor does he claim to be. What is he then? A philosopher of sorts, it is very clear he is interested most in being epistemologically honest.

In the video Taleb does make an interesting comment… if someone points to a house and says it is structurally unsound, does it matter if it falls down a minute later, or 10 years later? The house was unsafe.

He obviously takes the same idea with the economy or the markets — if it is unsafe, it doesn’t really matter if the market goes up at times… even for years at a time. That’s an idea that is antithetical to most traders, but traders don’t focus on the same things that philosophers do.

It’s also fun to watch the CNBC talking heads completely flummoxed and unsure how to even ask him questions.

Video via Ritholtz.

Fri 3 Jul 2009

Just found this, thought I’d share… Interactive Brokers (IB) has some free widgets (for both windows and mac) that gives you easy access to simple option tools. They basically help with the basics / fundamentals, but that is still pretty cool.

Download them for free here.

They would be cooler if the options calculator would automatically fill with option prices, but you have to have an IB account to have access to that stuff (it is available within IB’s trading platform).

Sat 27 Jun 2009

Below you will find the internal sales tactic sheet for Lehman Brothers traders salespeople. The brokers would use these sheets when talking to a customer or prospect, and use the canned responses to try and persuade them to do more business with the firm.

Take a gander, and think about whether or not your are swayed by the emotions they try to evoke… The takeaway is that brokers are first and foremost salespeople.

Mon 15 Jun 2009

From the 5 Minute Forecast:

Sign of the times: Name the best-selling car in the United States. Nope, not the Toyota Camry, although that?s a good guess. No, in these recessionary times the crown goes to…

No bailout money was used in the production of this automobile.

Yes, it?s the Little Tikes Cozy Coupe, a venerable model introduced in 1979 ? earning itself a permanent spot recently at the Crawford Auto-Aviation Museum in Cleveland.

With an MSRP of around $60, the pedal-powered single-seater sold more than 457,000 units last year ? more than any model of the gasoline-powered variety. It?s American-made in Hudson, Ohio, and free of the taint of bailout money or White House-engineered bankruptcy proceedings that hosed secured creditors.

Sun 31 May 2009

Fascinating stuff from Barron’s…

But a less-noticed intrigue occurs on the date when Russell measures stock-market caps to determine index membership. It is May 29 this year. Working as a trader at Morgan Stanley some years back, Rosenthal noticed stocks that surged suspiciously up the ranks on the day Russell took its snapshot. “People actually forced stuff in…that is just evil,” says the finance prof. “It isn’t like you figured something out, but that you made it happen.”

Those suspicions seem borne out by the data of Zhan Onayev and Vladimir Zdorovtsov, researchers at State Street who studied the past nine years of Russell reconstitutions. Among the stocks that just squeaked above the Russell 2000 threshold, a disproportionate share of the gains for May occurred on that measurement date — in- deed, in the last minutes of that day.

…Last year, about 200 new additions made it over the Russell 2000 threshold, which was the market cap of the 3000th stock at the close of May 30, 2008-or $167 million. In this year’s still-recovering market, analysts like Citigroup’s Lori Calvasina predict the cutoff will be down around $72 million. A would-be manipulator might hoard illiquid stocks with market caps under that level, in hope of pushing them up on May 29.

The easy way to curtail this sort of stuff would be to take the average market cap over a period of time (say, 6 months) as criteria for inclusion…

Kinda similar, Friday’s close was nothing short of spectacular. Karl Denninger has more over at his blog, but suffice it to say, a rather large order showed up in the futures for the SPX in the last minute (/ES is the S&P 500 e-mini futures contract). The total margin for the number of contracts pushed through was close to $22.5 million, with a dislocation that cost the order giver a whopping $1.25 million disadvantage for trying to push it through in the way they did.

I assume, and Dennninger agrees, that it was most likely a short position that got liquidated. But I think it raises more than a few eyebrows amongst those that are usually impervious to conspiracy theories…

Mon 25 May 2009

A friend was nice enough to send me a blog posting about the USD no longer being the Russian Reserve Currency. Shocking stuff, surely, but let’s take a look at the cited MarketOracle.co.uk article…

The US dollar is not Russia?s basic reserve currency anymore. The euro-based share of reserve assets of Russia?s Central Bank increased to the level of 47.5 percent as of January 1, 2009 and exceeded the investments in dollar assets, which made up 41.5 percent, The Vedomosti newspaper wrote.

The dollar has thus lost the status of the basic reserve currency for the Russian Central Bank, the annual report, which the bank provided to the State Duma, said.

In accordance with the report, about 47.5 percent of the currency assets of the Russian Central Bank were based on the euro, whereas the dollar-based assets made up 41.5 percent as of the beginning of the current year. The situation was totally different at the beginning of the previous year: 47 percent of investments were made in US dollars, while the euro investments were evaluated at 42 percent.

The dollar share had increased to 49 percent and remained so as of October 1. The euro share made up 40 percent. The rest of investments were based on the British pound, the Japanese yen and the Swiss frank.

The report also said that the reserve currency assets of the Russian Central Bank were cut by $56.6 billion. The losses mostly occurred at the end of the year, when the Central Bank was forced to conduct massive interventions to curb the run of traders who rushed to buy up foreign currencies. The currency assets of the Central Bank had grown to $537.6 billion by October 2008. Therefore, the index dropped by almost $133 billion within the recent three months.

The majority of Russian companies, banks and most of the Russian population started to purchase enormous amounts of foreign currencies at the end of 2008. The dollar gained 16 percent and the euro 13.5 percent over the fourth quarter. The demand on the US dollar was extremely high, and the Central Bank was forced to spend a big part of its dollar assets, experts say.

There’s another way to read the Russian currency reserves situation…

The Russian central bank didn’t change it’s reserve ratios because of some macro analysis, they did so because of the domestic demand for foreign currencies (specifically the USD) and their intention to defend their currency.

Last October, Russia had US$500b in currency reserves (I’m rounding to make the math easier but less precise), 49% of it in USD ($245b) and 40% in EUR ($200b).

At the beginning of 2009, Russians started trying to buy foreign currencies, “The demand on the US dollar was extremely high.” To defend their currency, Russia removed funds from their currency reserve to meet the foreign currency demand and keep the ruble from collapsing.

Within the last several months, the Russian foreign currency reserves dropped by $133b. Let’s say 80% of the demand was for USD (“extremely high”). That would be $106b of the amount the reserves fell. Let’s say the other 20% is EUR, or $27b.

After transferring out $106b of USD, the Russian reserve would have $139b in USD. After transferring out $27b in EUR, they would have $173b in EUR. After these transactions, the new % split for the currency reserve would be 38% USD and 47% in EUR (relatively close to the percentages cited in the article, close enough for my loose arithmetic).

Instead of being proof of low demand for the USD, this article is actually evidence of incredibly high demand for the USD.

I think I’ve said it before… the USD is the worst currency in the world, except for all the others.

Sat 23 May 2009

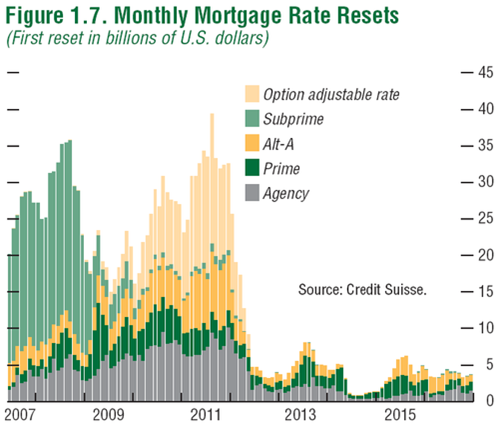

Think that we’ve finally reached the bottom of the housing market?

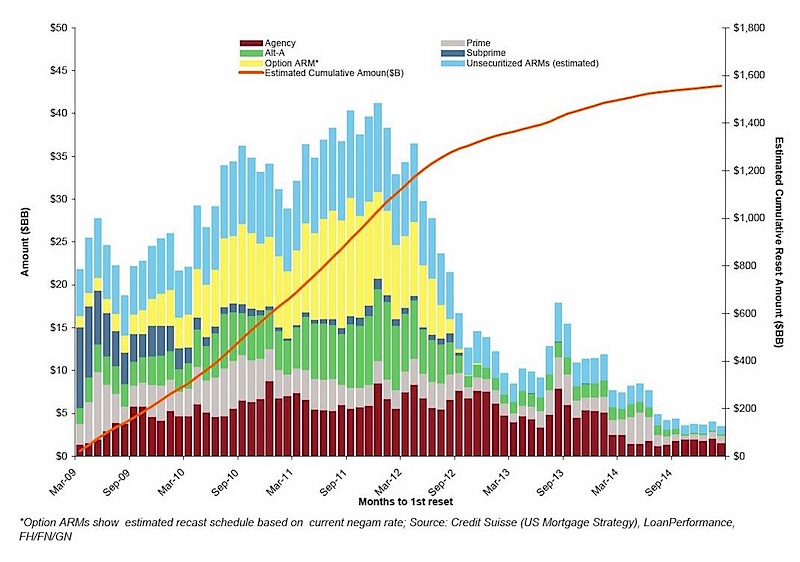

Let’s go back to how things looked in October 2007… we had a huge wave of subprime mortgages resetting, with a peak at about $35b (per month) in resets occurring in mid-2008. A majority of the resets were subprime.

And now the current situation, thanks to Calculated Risk:

Here we see another wave of resets coming, this time peaking at $40b in resets near the end of 2011. Subprime is a much smaller portion of the resets, but we still see between $20b and $25b of mortgages being reset every month through the rest of 2009 and 2010.

If mortgage rates stay low, this might not be a problem… but it doesn’t seem to me like we’re in the clear yet.

Sat 16 May 2009

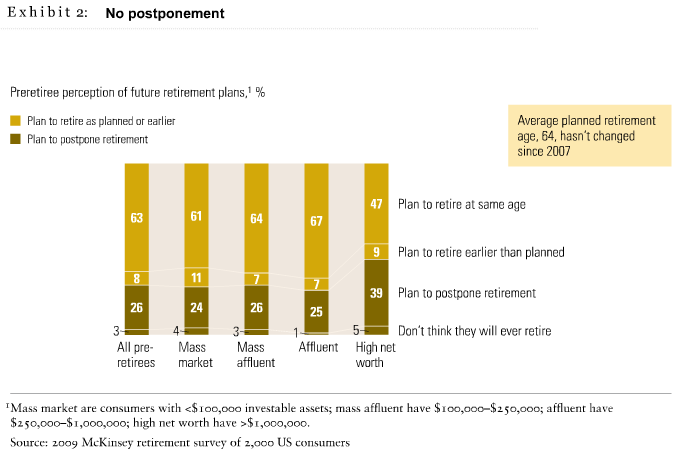

Proving that Denial isn’t just a river in Egypt, only 25% of pre-retirees are considering postponing their retirement age despite being woefully underprepared financially for retirement.

From a McKinsey Quarterly Economic Study:

Although consumers have taken some … steps, these could be masking a deeper failure to understand the state of retirement security. McKinsey?s retirement readiness index (RRI)?which uses Social Security, defined benefits, defined contributions, and other financial assets to measure the financial preparedness of households for retirement?is currently at 63 for an average household in January 2009. Consumers must have an RRI of 100 to maintain their current standard of living at retirement. An RRI below 80 calls for large reductions in spending on basic needs, such as housing, food, and health care.

Yet our survey showed that only about a quarter of US consumers are considering postponing retirement as a result of the crisis: the expected retirement age, 64, hasn?t changed since 2007 (Exhibit 2). Despite the fall in home values, the proportion of people planning to finance their retirement through home equity has increased slightly.

What is the prevailing attitude and what did these pre-retirees do about it?

…consumer anxiety about interest rate risks and a lack of guaranteed income has more than doubled, to around 60 percent, from the levels prevailing three to five years ago; worries about market and inflationary pressures have jumped by half, to about 75 percent…

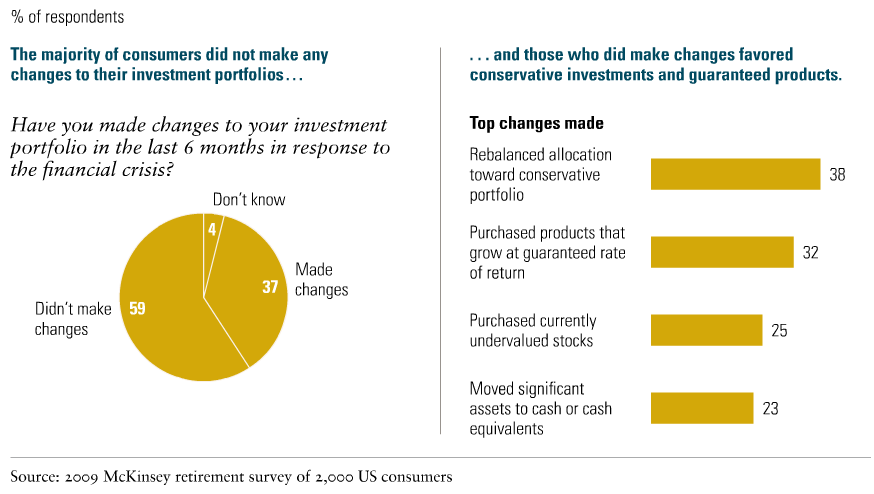

…in the past six months, only 1 percent have moved assets away from their primary financial institution, just 37 percent have changed their investment portfolios, and no more than 20 percent have changed their retirement portfolios. Those who did make changes have tried to reduce their risk levels by rebalancing allocations toward conservative assets (38 percent), products with guaranteed rates of return (32 percent), and holdings of cash and cash equivalents (23 percent) (Exhibit 1). Most preretirees have also responded to the financial crisis by curbing their lifestyles: some 60 percent reduced spending in the six months leading up to January 2009, and 73 percent paid down debt.

A separate nugget of blame from the same article:

…just 1 percent of preretirees hold their individual advisers primarily responsible for the impact of the crisis on them, compared with 43 percent who blame the government and regulators, and 27 percent who blame financial institutions.

I wonder who or what the other 30% blame?

Thu 14 May 2009

John Hussman has another great weekly letter this week, with many salient points. Read the whole thing and you won’t be disappointed.

Here are a few choice quotes:

Banks Pass Stress Test – Regulators Fail Ethics Test

Last week, financial stocks enjoyed a powerful advance and short squeeze on the announcement of the results of the ?stress test? of major banks. It is important to begin by noting that this was not a regulatory procedure with teeth. It was initially a response to Congressional demands to introduce greater objectivity into the use of public capital for these bailouts, and gradually morphed into nothing more than a ?confidence building? exercise. And keeping with the emphasis on keeping the numbers happy, as opposed to providing full and fair disclosure, the Wall Street Journal reported on Saturday, ?The Federal Reserve significantly scaled back the size of the capital hole facing some of the nation’s biggest banks shortly before concluding its stress tests, following two weeks of intense bargaining. In addition, according to bank and government officials, the Fed used a different measurement of bank-capital levels than analysts and investors had been expecting, resulting in much smaller capital deficits.?

…Now, just think of this for a minute. Even if you assume that the ?risk-weighted assets? of the banks are about two-thirds of their total assets (as the stress-test does), we’re still looking at $7.8 trillion in total assets at risk in these banks, and despite being on the edge of insolvency only weeks ago, we are asked to believe that they will need less than 1% of this amount ? $74.6 billion ? of additional capital even in a worst case scenario…

…Of course, Citi’s entire market cap is only $22 billion, so the ?$5.5 billion? that Citi is reported to need under the stress test is what it would require after a 5-to-1 dilution in its common stock (87+22/22). Essentially, we’ve got a company with a common equity buffer of just over 1% of total assets, that just 8 weeks ago was on the verge of receivership, and investors are urged to believe that there are enough voodoo dolls in the vault to make the company solvent even in a further weakened economy.

Hussman delves into more of the mechanics of the math, but arrives at this logical conclusion that everyone should have if the stress tests were actually to be believed:

Great. Then no more government money should be needed. Outstanding. Not a dime more of public funds beyond what remains in the TARP. No need to use public money to buy toxic assets either.

I for one heartily agree.